Mapping Versus Capital Budgeting

Preface: I’ve become obsessed with Wardley Maps. Wardley maps are true maps - that is, planes with direction and movement - that help you understand the implications of a business' strategy. If you’re not familiar with them, I recommend reading Simon Wardley’s WIP book on Medium or trying Ben Mosior’s Build your First Wardley Map.

Wardley maps have become an important part of my decision making toolkit. I use them to understand & communicate the strategic considerations of companies I interact with.

However, the strategic implications of Wardley maps can come into opposition with other decision making tools. Whenever we see contradictions from trusted rules, we must dive deeper - either one of our tools is broken, or we’re not seeing the whole situation.

In this post, I’ll consider what we’re missing when the Wardley Map contradicts a capital budgeting rule, like the IRR rule.

This post will assume you are familiar with Wardley Maps. It will also assume you understand the IRR rule. If you are unfamiliar with the IRR rule, see a brief explanation at the bottom of this post 1.

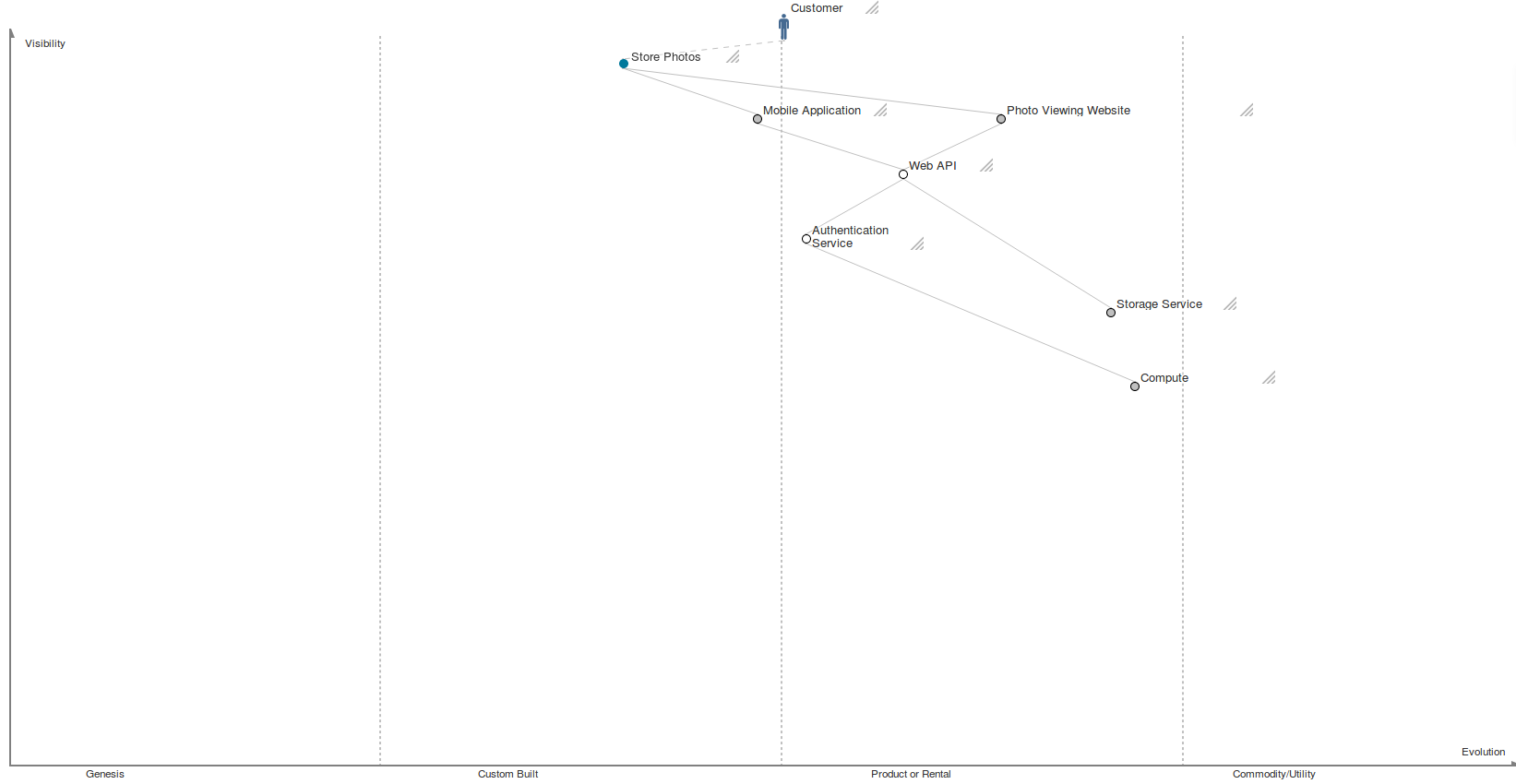

Let’s consider a real-life situation. Here’s an example map for, say, Dropbox, prior to them moving their storage services from S3 to a custom-built solution.

Let’s say we’re Dropbox, and we’re evaluating a proposal to invest significantly in building our own storage service, and move off of AWS. The IRR rule works out - at least on our projects, we can invest some reasonable amount, and save immensely on our AWS bills.

But building a custom replacement for Amazon S3 is replacing something that is at least a ‘product’, if not a utility, with a custom-build option. That is moving our dependency to the left on the Wardley map - against the grain of history! By doing so, we’ll lose out, or have to pay to keep up with, any benefits that would accrue naturally over time, as components move rightwards on the map.

Let’s assume that we’ve already negotiated as hard as we can against Amazon, and that we can’t get a suitable quote from any other provider (replacing S3 with another competing service would not imply changing our map, and so there would be no conflict, and negotiating well is just good business sense).

We appear to be in a dilemma: either (a) our Wardley Map is steering us wrong, and custom built is the way, (b) our IRR rule is no good, and we should keep paying Amazon for S3.

I propose that in this situation, our cost of capital is too low. We should find ways to increase our cost of capital, by adding risk, by developing new products, by buying back equity.

Consider how the cost of capital varies with the x-axis of the Wardley map. To the left, in the Genesis and Custom Built zones, we have high risk and high uncertainty. Our cost of capital is high. As we move rightwards, towards utilities, our cost of capital should decrease - building a new power plant can be done for practically zero cost of capital, with government bonds.

Consider Dropbox’s map above. Like maps for most companies, the end user need that is being fulfilled is leftwards of many of the internal dependencies. That is, the cost of capital for the business as a whole should be higher than the cost of capital for some of the internal dependencies, considered in isolation. If our cost of capital happens to be such that it looks like we can make profitable but non-strategic investments low in our value chain, it must be because our cost of capital is that of a more mature company than we actually are - and we should increase our cost of capital (share buybacks! dividends!) to compensate; not tilt the windmill of building a custom utility.

-

If you are unfamiliar, the IRR rule is this: when a company decides how to invest (that is, how to allocate or budget capital), it should consider each project’s Internal Rate of Return - that is, the expected return from the results of the investment - and compare it to the company’s cost of capital. If the IRR > Cost of Capital, then the project may be a good choice; if IRR < Cost of Capital, the project should not move forward. Fundamentally, the IRR rule expresses this: if the company makes this investment, do we expect to make profit in excess of our cost of capital? As an example, consider a company that makes TV remotes may consider to spend $1m on a new machine that will enable them to sell, after the cost of production and sales, an extra $200k’s worth of TV remotes each year for 5 years and then scrap the machine and recover $700k at the end of the 5th year. The internal rate of return of this project is 15.60%. If the company can borrow $1m from the bank for 7%, then 15.6% > 7%, and the investment should be made.↩